advocacy toolKIT

Advocacy toolkit for

The European Microfinance Network (EMN) offers an Advocacy Toolkit designed to assist its members in developing effective advocacy strategies at the national level. This toolkit provides practical resources to enhance communication with media, investors, policymakers, and other stakeholders, aiming to improve the regulatory and operational environment for microfinance institutions (MFIs) across Europe.

The European Microfinance Network (EMN) offers an Advocacy Toolkit designed to assist its members in developing effective advocacy strategies at the national level. This toolkit provides practical resources to enhance communication with media, investors, policymakers, and other stakeholders, aiming to improve the regulatory and operational environment for microfinance institutions (MFIs) across Europe.

Key components of the toolkit include:

- European Microcredit Whitepaper: A comprehensive 40-page document that introduces the European microcredit sector, exploring its definition, history, key figures, social and economic impact, and alignment with policymakers’ objectives. It concludes with policy proposals to enhance the framework for microcredit.

- Policy Notes and Position Papers: These documents address various topics such as market failures in microfinance, cost and pricing of microcredit, regulatory frameworks for microenterprises and self-employment, and proposals for EU financial instruments to support the sector.

- National Regulatory Fact Sheets: Detailed overviews of the regulatory landscapes for microfinance in different European countries, providing members with comparative information to support their advocacy efforts.

By utilising these resources, EMN members can effectively engage in advocacy activities, aiming to influence policy, enhance financial inclusion, and create a supportive environment for microfinance initiatives within their respective countries.

01The European Microcredit Whitepaper

The European Microcredit Whitepaper is a comprehensive 40-page introduction to the European microcredit sector. It explores its definition, its history, and key figures. It explores the social and economic impact, and sets out in which ways it achieves the policymakers’ objectives, and the ways in which the EU supports microcredit. At the end, it sets out a number of policy proposals that could globally improve the framework for microcredit.

The Whitepaper can hopefully help EMN members shape their own stories, to help them demonstrate the context, value, and goals of European microfinance, and help communicate these to policymakers and other stakeholders.

The whitepaper was published in July 2019 by a working group of the Parisian business association EUROPLACE, with EMN playing an active role in the shaping and delivery of the document. The working group included members of the French Central Bank, the banking association, and several financial service providers.

02 Microfinance in EU policies

EC Final Communication 2007: A European initiative for the development of micro-credit in support of growth and employment

In the beginning of the years 2000, in the EU, the microcredit sector in many Member States and regions was developing rapidly, and a number of actions were taken at Community level to reinforce the growth of the sector. However, there was clear evidence that much more can be done.

The EC elaborated this Communication, which set the basis for the different programmes and actions developed and under implementation by the EU institutions over the past decade. It proposes a European microcredit initiative focused on 4 main points:

Strand 1: Improving the legal and institutional environment in the Member States

Strand 2: Further changing the climate in favour of entrepreneurship

Strand 3: Promoting the spread of best practices

Strand 4: Providing additional financial capital for new and non-bank MFIs

European Pillar of Social Rights

The European Pillar of Social Rights is a manifesto setting out the principles of sustainable growth and the promotion of economic and social progress, as well as cohesion and convergence, while upholding the integrity of the internal market, to achieve efficient employment and social outcomes. It was agreed as a commitment made by the leaders of 27 Member States and of the European Council, the European Parliament and the European Commission in the Rome agenda, 2017.

European Pillar of Social Rights underpins all the work that the European Commission does, and particularly the work done in the social sphere by DG GROW.

For microfinance, the key is “Access to essential services: Everyone has the right to access essential services of good quality, including water, sanitation, energy, transport, financial services and digital communications. Support for access to such services shall be available for those in need.” Also, useful remarkable messages in Chapter I point 4 a. and c., Chapter II point 5 c. and Chapter III point 12

EU Social Economy Action Plan

In June 2023 the European Commission publishes its proposal for a “Council recommendation enabling framework conditions for social economy.

On November 27th, the Employment, Social Policy, Health and Consumer Affairs Council (EPSCO) adopted the Council Recommendation to enable the development of framework conditions for the development of social economy.

With this recommendation, Member States of the EU are asked to set up an enabling environment to allow the development of the social economy sector.

Sustainable Development Goals

The Sustainable Development Goals (SDGs) are an ambitious plan of action defining sustainable development priorities at a global level to 2030, with the aim of eradicating poverty and promoting decent lives with opportunities for all. There are 17 goals and 169 universal targets that are inter-connected, applicable to all nations and peoples, and that represent a call to action for governments, civil society and the private sector.

Microfinance, combining financial products and business development services, contributes and is an enabler to the improvement of several of the SDGs:

- SDG 8 “DECENT WORK” – Targets 3, 6, and 10. Encouraging entrepreneurship and inclusive job creation are key to ensuring everyone can contribute to the labour market with dignity. This in turn contributes to reducing extreme poverty, to growing the middle class, and to growing the economy.

- SDG 10 “REDUCE INEQUALITIES” – Targets 1, 2 and 4. Growing income inequalities require sound policies to empower lower income earners and promote the economic inclusion of all regardless of gender, ethnicity, age, disability, or religion.

- SDG 4 “QUALITY EDUCATION” – Targets 4 and 5. Teaching financial literacy at all ages contributes to eliminating gender and wealth disparities and encourages universal access to productive economic participation. Microcredit leverages support, coaching, mentorship to ensure clients have the necessary skills to succeed in business.

Transition Pathway for the proximity and social economy for a green and digital transition

As part of the Transition pathway, EMN and its members submitted 2 pledges in February 2023:

- The first one on how to create financial incentives and supportive regulation for green and circular social economy business models;

- The second one on the development on digital platforms to scale up access to finance

03Demonstrating the social and economic impact of microfinance

Impact studies examples

Qredits published its 2018 Social Annual Report demonstrating their contribution to the economy, employment and the reduction of welfare beneficiaries. It has a definite impact on the society, with 12,000 entrepreneurs financed, 25,000 jobs created, €47 million in government savings in social welfare, 87% survival rate after 3 years, 7% of customers employ partially disabled or people on welfare and 19% of companies work with volunteers. In addition, in October 2019 Qredits has developed a new loan product for social enterprises.

MicroBank 2019 Annual Report illustrates the impact on the entrepreneur and his/her family environment: 81% improved their management ability, 69% improved liquidity, for 46% income level have increased, in terms of individual well-being 97% feel capable and valuable in their daily lives, 90% find their work fulfilling and 52% integrate some form of environmental good practices. Moreover, MicroBank managed to show its impact for business consolidation (74% of entrepreneurs feel that their business has been consolidated as a result of the loan), for job creation (microcredits directly contributed to the creation of 20,174 jobs and businesses that received a microcredit directly created an average of 1.2 jobs) and for wealth generation in the area (total of 56,836 jobs in Spain were linked to the activities of the businesses funded by MicroBank and making a contribution to the GDP of €1,543 million).

PerMicro is another organisation giving a key role to the social impact of their products/services, elaborated the report measuring impact for enterprises and for families in 2018. PerMicro contribution to job creation and strengthening employment is demonstrated in the report: in average every enterprise supported by PerMicro created new job positions (60% are young people, 23% migrants, 46% women and 48% unemployed). In terms of economic-social welfare and poverty reduction, 46% of entrepreneurs improved their quality of life and 47% of entrepreneurs have an average income higher than 608€/month, 2,5% of families crossed over the poverty line and 29% of people no longer live in conditions of sever material deprivation as previously declared. Finally, the component of empowerment of women is also mentioned, 58% of customer of microcredits for families were female, the majority of them are migrants, 11% young women under 35 and half of them has more than one child.

EMN has collected more examples here, and a systematic approach in the impact measurement and management assessment can be found in the following paper of Microfinanza srl published in May 2020.

Social Return on Investment method

If we consider that microfinance gives people opportunities to create their own employment, the calculation of the impact of microfinance should also calculate how much it saves the welfare system, and how much taxable value it generates.

Adie, together with KMPG, developed the Social return on Investment (SROI) method. The return on investment is, in short, revenue generated for society, and costs avoided by society thanks to Adie’s work. The SROI method allows us to put a number on the revenue generated and costs avoided. The result of the SROI work shows that investment in microfinance products has a positive leverage on public budgets, €1 invested in Adie’s professional microcredit programme, that is the work with entrepreneurs, generates a revenue of 2,38 EUR in 24 months of time.

microStart in Belgium did a similar exercise and identified 3 different socio-economic impacts generated: a) The savings for the Belgian government in their social benefits programs; b) The additional revenues for the Belgian treasury generated by the activities of microStart’s clients; c) Enhancement of local economies and economic inclusion of communities. For every €1 microStart grants as a loan, the government adds €1.31 to its budget.

MEMI project

The project seeks to provide policy makers with the evidence-based policy recommendations capable of strengthening further the role of microfinance as one of the strategic tools to obtain financial and social inclusion in the EU.

“Measuring Microfinance Impact in the EU. Policy Recommendations for Financial and Social Inclusion” is a three-year (2016-2019) research project which has been financed by the EIB Institute and supervised by the EIF. The main aim of the research project is to assess the impact of microfinance compared to that of welfare programmes, on financial and social inclusion to establish which one ensures the higher social return.

3 Working Papers have been published as a results from this MEMI project:

- “Evaluating the impact of European microfinance. The foundations“

Working Paper 2016/033 sets out what can be learned from impact evaluations in developing countries, it takes a glance to challenges of impact evaluations, strengths and weaknesses of the various impact evaluation methods available, methodological options and provides an informed ground to make methodological decisions. - “The social return on investment (SROI) of four microfinance projects“

Working Paper 2020/065 introduces and applies – in the form of case studies – a specific methodology, SROI, to measure the impact of microfinance on financial and social inclusion. - “Measuring microfinance impact: A practitioner perspective and working methodology“

Working Paper 2020/066 complements the SROI methodology by introducing an analytical approach, which relies on indicators concerning the three dimensions, i.e. economic, social and environmental.

04 Overview of EU available funding resources

Employment and Social Innovation (EaSI) Programme

The EaSI programme is an EU financing instrument to promote a high level of quality and sustainable employment, guaranteeing adequate and decent social protection, combating social exclusion and poverty and improving working conditions (2014-2020). It has three main axes. The Microfinance and Social Entrepreneurship axis: with the objective of supporting access to microfinance and social entrepreneurship, had 3 types of instruments of funding: a guarantee instrument, capacity building and a funded instrument.

The EaSI Guarantee is available until September 30th 2023. For more information you can check the website of the European Investment Fund.

InvestEU programme

According to the European Commission assessment, the EaSI programme has proven the capacity of EU-level financial instruments to deliver the objectives envisaged by the EU regulation for micro-finance and social entrepreneurship, therefore justify its continuity and need for additional firepower.

The success of the EaSI programme led to the pursuit of objectives through a new tool, the InvestEU programme which is part of the 2021-2027 Multi-Financial Framework (MFF). The InvestEU program aims at supporting sustainable investment, innovation and job creation in Europe.

The program consists of three components:

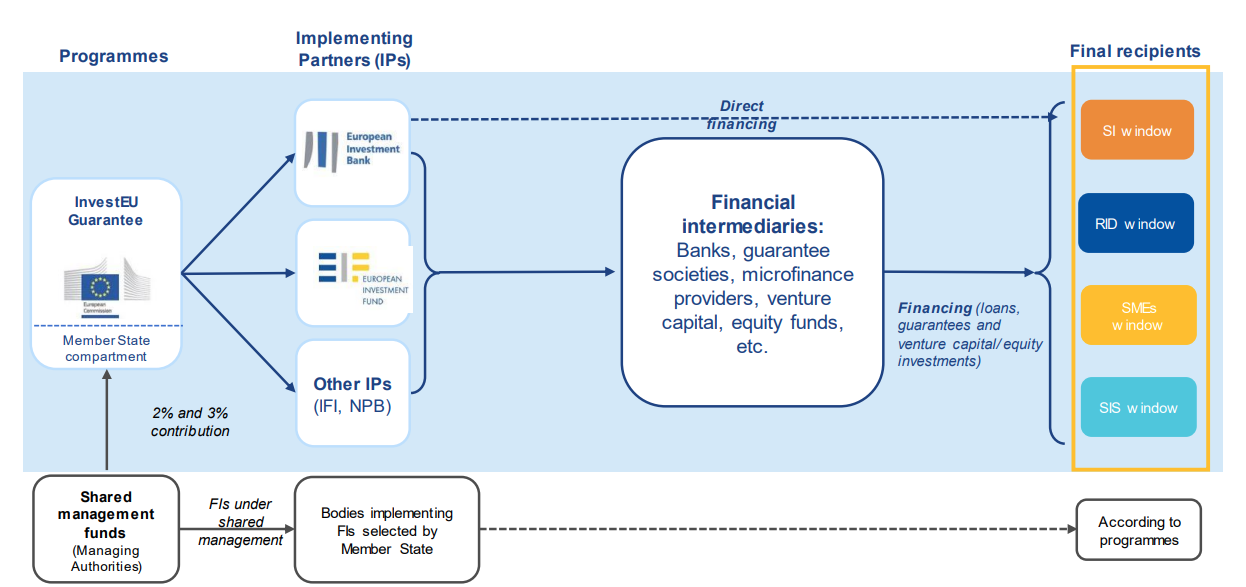

1. InvestEU Fund

With an EU budget guarantee of EUR 26.2 billion backing investments from implementing partners, the InvestEU Fund will support four windows:

- Sustainable infrastructure: financing projects in sustainable energy, digital connectivity, transport, the circular economy, water, waste

- Research, innovation and digitalisation: financing projects in research and innovation

- Small and medium-sized companies: facilitating access to finance for small and medium-sized companies

- Social investments and skills: financing projects in skills, education, training, social housing, schools, universities, hospitals, social innovation, healthcare, long-term care, accessibility, microfinance, social enterprise, integration of migrants, refugees and vulnerable people.

In March 2022, the European Commission, EIF and EIB (the main implementing partners) signed the Guarantee Agreement which is covering 75% of the EU guarantee. The guarantee is also open to other international financial institutions and promotional banks such as the European Bank for Reconstruction and Development (EBRD), the Council of Europe development Bank (CEB) and the Nordic Investment Bank (NIB).

The Council of Europe Development Bank (CEB) is providing loans to microfinance institutions and social finance providers to finance vulnerable entrepreneurs and to support their social inclusion.

Source: European Commission

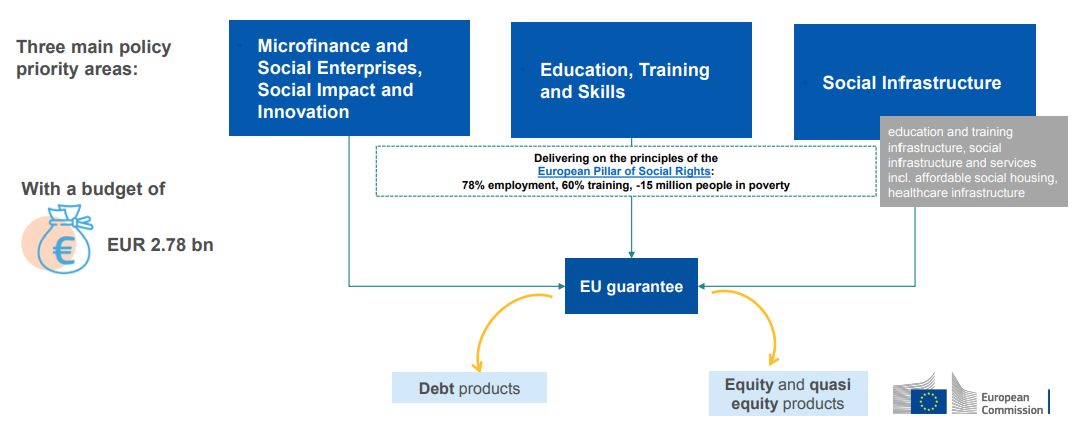

Microfinance is part of the last window with a budget of EUR 2.78 billion and three main policy areas: 1) Microfinance and social enterprises, social impact innovation, 2) Education, training and skills and 3) social infrastructure.

Source: European Commission

Under InvestEU, EIF launched a guarantee products for financial intermediaries

- SME Competitiveness guarantee

- Sustainability guarantee

- Innovation and Digitalisation guarantee

- Cultural and Creative guarantee

- Microfinance and Social Entrepreneurship guarantee

- Skills and Education guarantee

You can find more information on EIF guarantee products here.

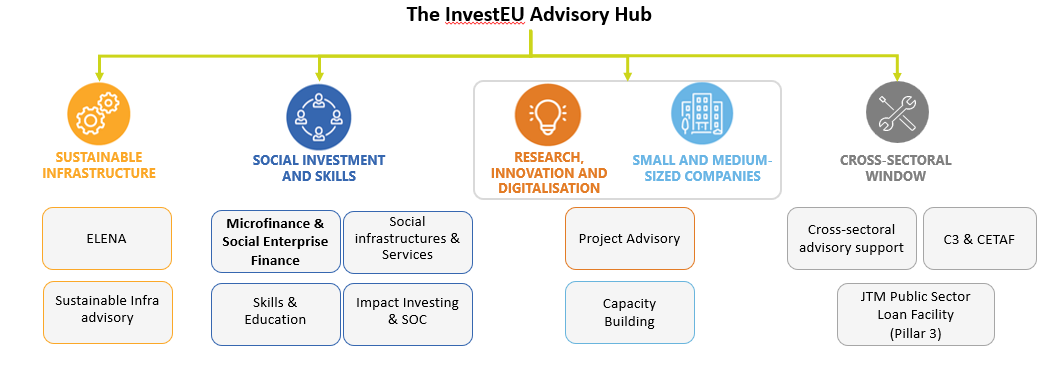

2. InvestEU Advisory Hub

The advisory Hub provides technical support and assistance for entities involved in the preparation, development, structuring and implementation of investment projects.

3. InvestEU Portal

The portal brings together investors and project promoters on a platform

Technical assistance under InvestEU

The technical assistance provided under the EaSI (Employment and social innovation programme) is now part of the InvestEU Advisory Hub. The new programme called SIFTA, managed by EIB, will provide targeted capacity building, project advisory and market development support to financial intermediaries active in the microfinance and/ or social entrepreneurship spaces.

Source: European Commission

Available in the 27 EU members states, the initial programme is open until December 2024. The program is open to microfinance providers such as banks and non-bank microfinance institutions and social enterprise finance providers such as investment funds, impact investors, incubators, accelerators that offer financial support to social enterprises.

SIFTA services (project advisory, capacity building and market development services) will be performed by a consortium of three organisations: Frankfurt School of Finance and Management (Consortium Leader), Microfinance Centre (Consortium Partner) and European Microfinance Network (Consortium Partner).

Information about SIFTA services are accessible here. Applicants of microfinance and social enterprise finance providers can apply for specific SIFTA services by sending an email to sifta@eib.org.

European Social Fund (ESF)

- Consult existing Operational Programmes in your country/region

- Check out funded projects in your country

- Plan ahead for your involvement in future ESF activities:

- Get in contact with your Managing Authority to get relevant information on the preparation of Partnership Agreements in your country (e.g. how to participate in official public consultations ahead of drafting the Partnership Agreements, which body is in charge of the consultation, or what is the timing? etc.) and to create awareness of the potential of microfinance in meeting ESF goals on employment.

- Consult examples of communications addressed to national government and regional managing authorities during the preparation of Partnership Agreements and OPs 2014-2020 that can be updated in view of the next ESF programming period.

- Advocate for your Managing Authority to set up a microcredit financial instrument as promoted by fi-compass. Fi-compass also offers several days of technical assistance to managing authorities, to give them tailored training in setting up financial instruments. Make your managing authority aware that this assistance is available for them.

An analysis of the role of microfinance using European Social Fund (ESF) funding has been performed by Microfinanza srl, selecting 5 case studies study in Spain, Italy, Poland, Belgium and Bulgaria. The primary market failures identified are related to: complexity, time consuming, lack clarity on the application process, reduced availability of information, strict eligibility criteria, limited awareness of Managing Authorities, no common policy for long-term commitment or focus on specific topics and lack of cohesion around the strategy of national policies and Managing Authorities. For a deeper understanding and overview, do not hesitate to consult this report.

European Social Fund plus (ESF+)

ESF + implementation

Source: European Commission

ESF + has a budget of EUR 87.9 billion for the period 2021-2027, out of which EUR 87.3 billion for the shared management strand implemented by the EU Member States (including ESF + Technical Assistance) and EUR 676 million for the EaSI strand. The European Social Fund plus will pursuit the work undertaken with the European Social Fund on EU’s employment, social, education and skills policies.

The new ESF + will merge the previous European Social Fund (ESF), Youth Employment (YEI), Fund for European Aid to the Most Deprived (FEAD), EU Health programme and employment and social innovation (EaSI) programme.

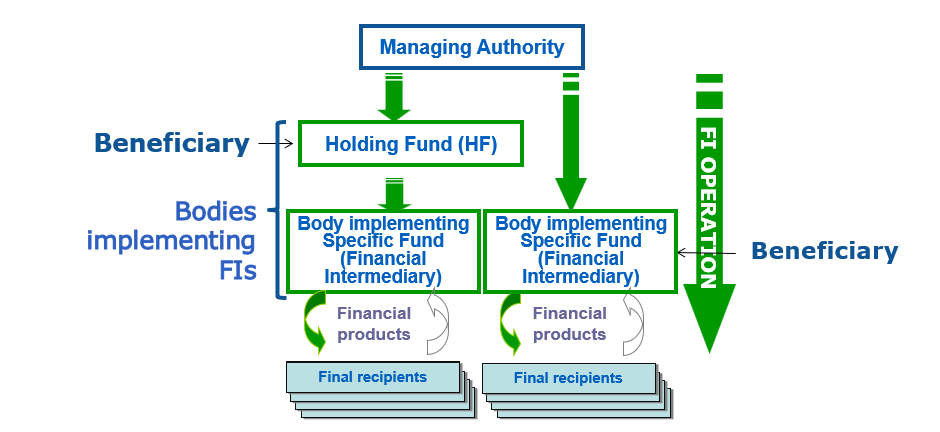

The implementation of the ESF + is mostly executed by the Managing Authorities in the shape of what is called “shared management”. A small part of the budget will also be centrally managed by the European Commission (EaSI Ta programme).

To receive support from the ESF + we recommend to:

- Get in contact with your Managing Authority to get relevant information on the preparation of Partnership Agreements in your country (e.g. how to participate in official public consultations ahead of drafting the Partnership Agreements, which body is in charge of the consultation, or what is the timing? etc.) and to create awareness of the potential of microfinance in meeting ESF goals on employment.

- Advocate for your Managing Authority to set up a microcredit financial instrument as promoted by fi-compass. Fi-compass also offers several days of technical assistance to managing authorities, to give them tailored training in setting up financial instruments. Make your managing authority aware that this assistance is available for them.

An analysis of the role of microfinance using European Social Fund (ESF) funding has been performed by Microfinanza srl, selecting 5 case studies study in Spain, Italy, Poland, Belgium and Bulgaria. The primary market failures identified are related to: complexity, time consuming, lack clarity on the application process, reduced availability of information, strict eligibility criteria, limited awareness of Managing Authorities, no common policy for long-term commitment or focus on specific topics and lack of cohesion around the strategy of national policies and Managing Authorities. For a deeper understanding and overview, do not hesitate to consult this report.

05Improving the national regulatory frameworks

In order to create a healthy atmosphere for microfinance, it is essential that it can rely on an enabling environment for entrepreneurship and self-employment. In most jurisdictions there is still work to be done to improve the framework conditions for self-employment.

To determine which regulatory aspects of self-employment are most crucially blocking progress in your country, you can self-evaluate using the following tools:

- OECD “Better Entrepreneurship” self-assessment tool. This online self-assessment tool can be used as a starting point for dialogues with government officials, to agree on where improvements can be made in the supporting environment for entrepreneurship.

- OECD “The Missing Entrepreneurs” publication gives country-by-country policy recommendations.

- This Economist Intelligence Unit article sets out a range of influencing conditions.

EMN performed the exercise of analysing the regulatory environment for microfinance in most European countries, elaborating legislative mapping reports per country. Members can use these reports as a basis for orienting their own efforts. In addition, MFIs can also take a look to the microcredit regulation overview report for past year. This paper can be a practical tool to compare their context with that of their peers across Europe, learning from their challenges and engage in discussion with policymakers on regulatory issues.